For half a century, the ascent from poverty to prosperity followed a well-trodden path. Nations built factories, harnessed cheap labor, exported their way to wealth, and watched as a middle class blossomed. This was the story of post-war Japan, the East Asian “Tiger” economies, and, most monumentally, China. Now, for the diverse nations of the Association of Southeast Asian Nations (ASEAN), this reliable route looks increasingly treacherous, perhaps even like a dead end. The region finds itself caught in a geopolitical pincer movement of unprecedented force: on one side, an increasingly protectionist and unpredictable America, and on the other, an economically assertive China whose sheer scale both buoys and batters its smaller neighbors. This superpower squeeze is not merely a diplomatic headache; it is an economic shift that is forcing a fundamental rethink of the very model that once promised a brighter future.

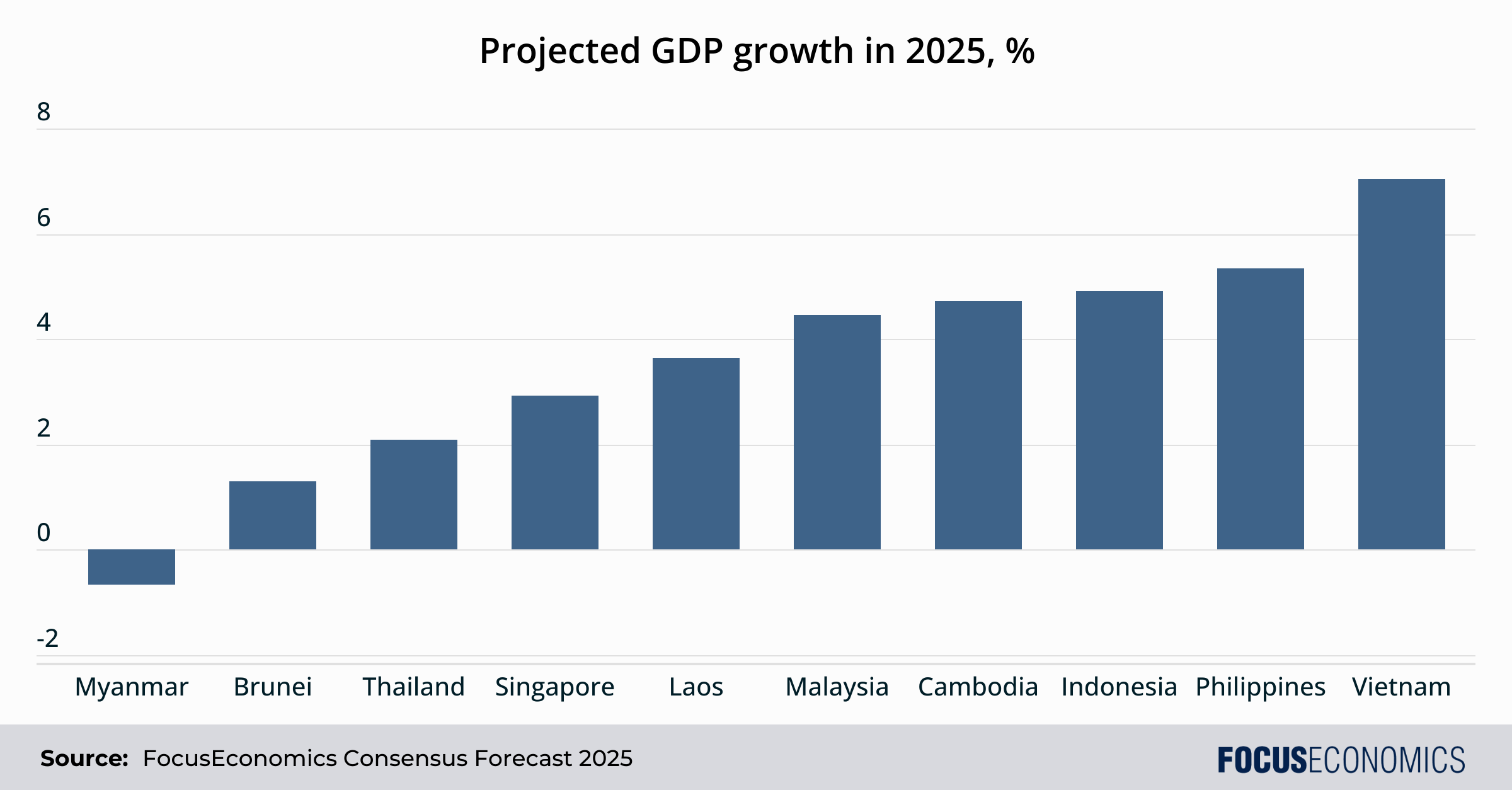

Recent GDP Growth in Southeast Asia

The economies of Southeast Asia have demonstrated resilience in clawing their way back from the Covid-19 pandemic. Regional GDP growth is projected by our panelists at 4.4% for 2025, well above the global and emerging-market averages, after averaging 4.6% from 2021 to 2024. That said, growth remains substantially below its pre-Covid trajectory, partly due to a comparatively sluggish Chinese economy.

There is substantial divergence amongst regional economies. For instance, while Myanmar is forecast to contract for the second straight year in 2025 due to ongoing civil conflict, Vietnam should be one of the world’s fastest-growing economies thanks to booming electronics exports.

Inflation, Exchange Rates and Interest Rates

In recent years, inflation has been muted by global standards. This is linked to large regional manufacturing capacity, domestic economic slack and an influx of low-cost goods from China. As a result, central bank interest rates have also been low by global standards. Regarding exchange rates, most ASEAN currencies are forecast to strengthen this year, before trading broadly sideways in 2026.

Trade With The U.S: Tariffs, Deals, and Strategic Investment

The return of a Trump administration in 2025 has meant that Southeast Asia, which had for a few years benefited from supply-chain diversification away from China, suddenly found itself in the crosshairs of Trump’s “America First” trade doctrine. After a baseline 10% global tariff was introduced in Q2, most countries in the region were hit by U.S. “reciprocal” tariffs in August. Malaysia, Indonesia, the Philippines, Thailand, and Cambodia were saddled with 19% rates. Vietnam, a key node in global electronics and apparel supply chains, secured a 20% rate. Laos’ exports to the U.S. were hit by a 40% surcharge.

These rates were in many cases lower than initially threatened levels, but only via significant concessions. These included commitments to purchase billions of dollars in American agricultural goods, commercial aircraft and energy products; to eliminate their own tariffs on most U.S. imports; and to dismantle a host of non-tariff trade barriers that had long frustrated American exporters. In a particularly telling move, Malaysia also pledged a hefty USD 70 billion in new capital investment in the United States.

So far, U.S. protectionism is yet to prove a significant headwind to south-east-Asian exports, for numerous reasons. Firms have frontloaded sales in anticipation of higher levies; adding to this, some goods showing up as regional exports are transshipments from China ultimately bound for the U.S. Moreover, some firms exporting to the U.S. have likewise rerouted goods via Canada and Mexico to stave off tariffs. And global demand for electronics—a key export for several Southeast Asian economies—has been strong. As a case in point, in January–September, goods exports from Indonesia, Singapore and Thailand—the three largest in the region—increased 6%, 11% and 14% respectively in annual terms.

On transshipments, Nomura analysts said:

“One crude but straightforward way to estimate which countries are the most affected by the transshipment of China-made products into the US is to calculate the correlation between the third country’s export growth to the US and its import growth from China on a 24-month rolling basis. We compute these correlation coefficients for 22 countries.[…] Unsurprisingly, ASEAN countries have among the highest correlation, especially Vietnam, Thailand, Malaysia and Indonesia.”

Regarding countries’ ability to circumvent tariffs, our panelist EIU said regarding Vietnam:

“Manufacturing sector growth [has recently] outperformed the consensus expectations by a large margin. This is in part due to still resilient exports to the US, along with a sharp increase in exports to countries such as Mexico and Canada. This substantial export surge possibly reflects Vietnamese manufacturers’ strategic pivot to Mexico or Canada as a way to potentially access US markets under more favourable US-Mexico-Canada Agreement (USMCA) terms. While both Mexico and Canada face new border- and fentanyl-related tariffs, exemptions for USMCA-compliant goods—such as electronics, pharmaceuticals and semiconductors—remain accessible. The expanded market penetration in Canada and Mexico is boosting total export earnings, cushioning volatility from US-bound flows.”

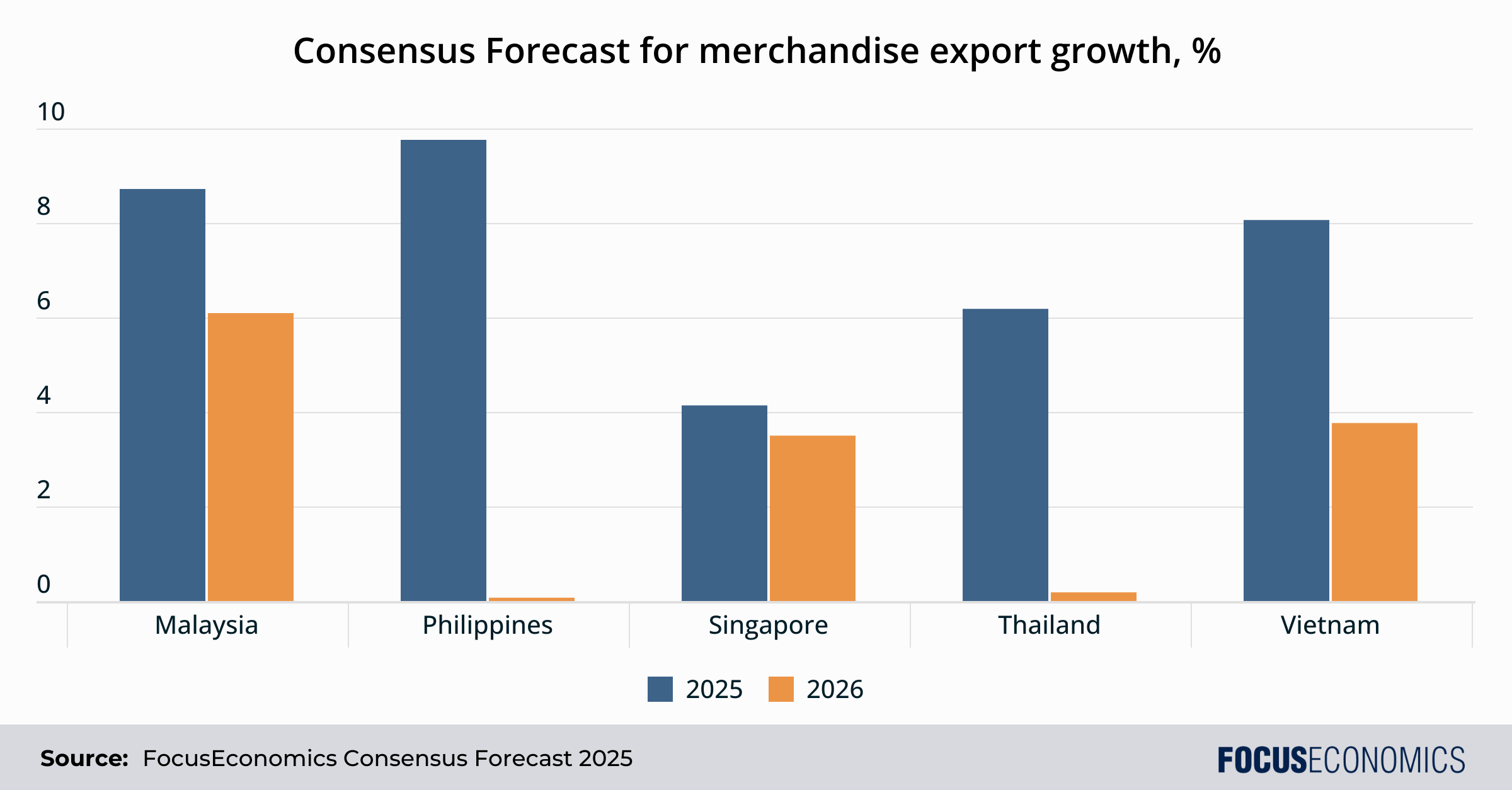

That said, this positive performance is unlikely to last. Frontloading will fade going forward. The White House is attempting to crack down on transshipments; the deal with Vietnam, for example, includes a punitive 40% tariff specifically on goods deemed to be illicitly rerouted. In any case, rerouting goods via ASEAN has lost appeal due to abating U.S.-China trade tensions. Moreover, with the exception of high-income Singapore, the region’s labor-intensive exporters don’t have the necessary margins to absorb tariff costs, leading to higher prices that could feed through to lower demand in time.

In line with this, our panelists see a notable slowdown in export growth in key Southeast Asian economies next year compared to 2025, as the graph below shows:

On the troubles facing firms, our panelist Nomura said:

“Higher US tariffs have left Asian exporters with a difficult choice: either pass on the rising costs and put US market share at risk, or absorb the costs and take the hit in profitability. This has been aggravated by local currency appreciation and competitive price pressures. Economies with higher-value, brand-driven exports tend to hold prices steady for longer, sacrificing margins, whereas low-margin exporters make a quicker move to pass on costs, risking competitiveness. If Asia’s profit margin squeeze worsens, we may see spillovers into the real economy. Exporters facing sustained margin pressure may cut back on capex, slow hiring or limit wage growth in export-dependent economies, which raises the risk of a negative feedback loop between trade shocks and domestic demand. This would require Asian policymakers to respond through targeted subsidies, tax relief or even currency intervention, if competitiveness erodes further.”

Even while wielding the stick of tariffs, Washington is also dangling the carrot of strategic investment. The United States remains, by a significant margin, the largest source of foreign direct investment (FDI) in ASEAN. The stock of U.S. investment into the bloc soared to an unprecedented USD 476 billion in 2023, a figure that dwarfs American investment in China, Japan and Korea combined. This is not passive portfolio investment; it is hard capital pouring into the factories and services that form the backbone of the region’s modern economy. American firms are market leaders in the region’s burgeoning semiconductor, finance and digital sectors. Intel is investing USD 7 billion in a new advanced packaging plant in Malaysia; Google and Microsoft are building data centers across the region; major American banks are expanding their operations in Singapore.

Furthermore, Washington is pursuing strategic framework agreements, such as those with Thailand and Malaysia, aimed at diversifying supply chains for critical minerals like rare earths. This is a clear geopolitical move to hedge against China’s chokehold on these essential resources. This dual approach—punitive tariffs on one hand, strategic investment on the other—has left Southeast Asia walking a tightrope. It has made China’s overtures of a stable, predictable partnership appear increasingly attractive.

Trade With China: A Flood of Goods and a Strategic Upgrade

As America raises its drawbridge, China is rolling out the red carpet. For years, ASEAN has been China’s largest trading partner, a relationship built on a foundation of geographic proximity and deep integration into regional supply chains. Bilateral trade soared from just under USD 200 billion in 2008 to nearly USD 1 trillion by 2024. This deep economic entanglement was further institutionalized and given a strategic upgrade in late October 2025 with the signing of the “Version 3.0” of the ASEAN-China Free Trade Agreement (ACFTA).

Hailed as a “milestone” by regional leaders, the upgraded pact is a forward-looking agreement that expands cooperation into the domains that will define the 21st-century economy: The digital economy, green technology and supply chain connectivity. Moreover, the ACFTA 3.0 provides a legal and administrative framework to facilitate firms moving final assembly and other value-adding processes to Southeast Asia—a key aim of regional leaders. For instance, the pact makes it easier, cheaper and faster for a product assembled in Malaysia with Chinese components to be legally certified as “Made in Malaysia.” For Beijing, the deal is a powerful piece of economic statecraft—a clear effort to position itself as the champion of open, rules-based trade, contrasting what it portrays as American protectionism and unilateralism.

But this warm embrace has a suffocating quality. As Chinese manufacturers face growing barriers in Western markets, they are diverting a torrent of goods into the relatively open markets of Southeast Asia. This influx is creating what many local businesses and labor unions decry as unfair competition, threatening to de-industrialize parts of the region before they have a chance to fully develop. This is no longer just about Chinese components being fed into regional assembly lines. It is a flood of finished products—from steel and solar panels to textiles and toys—often sold at prices that local producers simply cannot match. The rise of Chinese-owned e-commerce platforms like TikTok Shop and Temu has accelerated this trend, allowing Chinese factories to sell directly to Southeast Asian consumers, bypassing local distributors and retailers entirely.

The consequences for domestic industries are already being felt. In Indonesia, the textile industry, a major employer, is reeling: Hundreds of factories have closed since 2023, and hundreds of thousands of jobs are at risk. In Thailand, industry groups report that thousands of factories in sectors from steel and plastics to furniture and auto parts have been forced to shut down in recent years, partly due to an inability to compete with the wave of low-cost Chinese imports. In response, governments are being pushed to act. Countries like Vietnam and Indonesia have begun to impose their own anti-dumping duties and safeguard tariffs on a growing list of Chinese products, a sign of mounting friction beneath the surface of official bonhomie.

Can Southeast Asia Still Get Rich by Making Things?

For generations, the factory was the gateway to modernity. The manufacturing sector provided a crucial stepping stone on the development ladder, absorbing large numbers of unskilled and semi-skilled workers from the countryside, earning vital foreign currency through exports, and fostering a culture of technological learning and industrial upgrading. But in the 21st century, that tried-and-tested model is under strain. The relentless advance of automation and robotics means that modern factories, from semiconductor fabrication plants to automotive assembly lines, require far fewer workers than their predecessors. The “great unbundling” of global supply chains is giving way to a more fragmented and regionalized system, where resilience and proximity are prized as much as low costs. And looming over all is the sheer, unassailable dominance of China in many manufacturing sectors that ASEAN would itself like a bigger slice of, from consumer electronics to heavy machinery.

Despite this challenging backdrop, governments across Southeast Asia are refusing to give up on their dream of industrialization, and are often using the power of the state to nurture national champions and force their way up the value chain. The most audacious and consequential of these experiments is unfolding in Indonesia—a country blessed with the world’s largest reserves of nickel, a critical component in electric vehicle (EV) batteries. The government banned the export of raw nickel ore in 2020, presenting foreign companies with a stark choice: Build smelters and processing plants on Indonesian soil, or lose access to the resource entirely.

The results have been dramatic. The policy has triggered a massive wave of foreign investment, predominantly from Chinese firms, which have poured tens of billions of dollars into building a sprawling nickel processing industry from scratch on islands like Sulawesi. As a result, Indonesia’s nickel-related exports have skyrocketed from just over USD 3 billion in 2017 to USD 39 billion in 2024.

However, the move has created a profound dependence on Chinese capital, technology and labor, with most of the country’s nickel processing facilities dominated by Chinese firms. The environmental toll has been immense, marked by widespread deforestation, the challenge of managing vast quantities of toxic waste, and a heavy reliance on captive coal-fired power plants to run the energy-intensive smelters.

So if the manufacturing path is so fraught with difficulty, what is the alternative? A growing chorus of economists and policymakers points towards services. Across the developing world, the services sector now plays a much larger role in driving growth and employment than it did for earlier industrializers. Sectors like finance, software development, tourism and business-process outsourcing (BPO) offer a potential route to higher productivity and better-paying jobs. The Philippines has successfully built a world-class BPO industry for instance, leveraging its large, English-speaking workforce. Singapore has transformed itself into a global hub for finance, logistics and high-tech services.

But this path, too, is steep and strewn with obstacles. To succeed in services requires a more skilled, knowledge-intensive workforce. ASEAN’s digital infrastructure, while improving, remains patchy and uneven, particularly outside of major urban centers. A thicket of fragmented national regulations on everything from data privacy to professional licensing impedes the creation of a true regional single market for services, raising costs and complicating cross-border operations. To top it all off, even if regional economies deal with the aforementioned challenges, they may find that AI snatches away some or all of the jobs currently on offer.

Regional Business Development

Though Southeast Asia is predominantly a production base for foreign multinationals, it is also giving rise to its own corporate champions. This is most visible in the emergence of a flock of “unicorns”—privately held technology companies valued at over USD 1 billion.

To be sure, Southeast Asia’s unicorn population remains small when set against the global giants. As of mid-2025, the United States led the world with over 700 unicorns, a testament to its deep venture capital markets and unparalleled innovation ecosystem. China followed with around 300, and India had firmly established itself as the world’s third major startup hub with nearly 120. Europe, led by the United Kingdom and Germany, also boasted a significant and growing stable.

In contrast, Southeast Asia’s tally is more modest, numbering in the dozens, with the city-state of Singapore serving as the primary hub for fundraising and headquarters. Yet, the companies that have achieved this status are not mere imitations of their Western or Chinese counterparts. They are a telling indicator of the region’s unique strengths and the specific problems its innovators are trying to solve. Unlike the global B2B software giants of Silicon Valley or the deep-tech hardware firms of Shenzhen, Southeast Asia’s unicorns are overwhelmingly consumer-focused, building platforms that address the everyday needs of a young, mobile-first population.

The most successful ventures are those that have tackled the region’s logistical and financial frictions. In the sprawling, archipelagic markets of Indonesia and the Philippines, logistics has been a formidable challenge. Homegrown companies like Indonesia’s J&T Express and Singapore’s Ninja Van have built vast, tech-enabled delivery networks tailored to these unique geographies, outmaneuvering global competitors with their local knowledge and operational agility.

In financial technology (fintech), a wave of startups has emerged to serve the millions of people who are “unbanked” or “underbanked” by traditional financial institutions. Companies like GCash in the Philippines, MoMo in Vietnam and Ascend Money in Thailand have become indispensable parts of daily life for locals. They have evolved from simple mobile payment apps into comprehensive financial “super-apps,” offering a suite of services that includes loans, insurance and investment products directly through a smartphone. With over 80 million registered users, GCash is on track for what could be one of the largest IPOs in Philippine history, a sign of the immense value being created in this sector.

In the fiercely competitive world of e-commerce and ride-hailing, regional giants like Indonesia’s GoTo and Singapore’s Grab have become dominant players, successfully building integrated ecosystems that combine transportation, food delivery and financial services. Traveloka, an Indonesian online travel platform, has become a regional powerhouse by demonstrating a deep understanding of local travel patterns and preferences.

Southeast Asia’s Economic Outlook

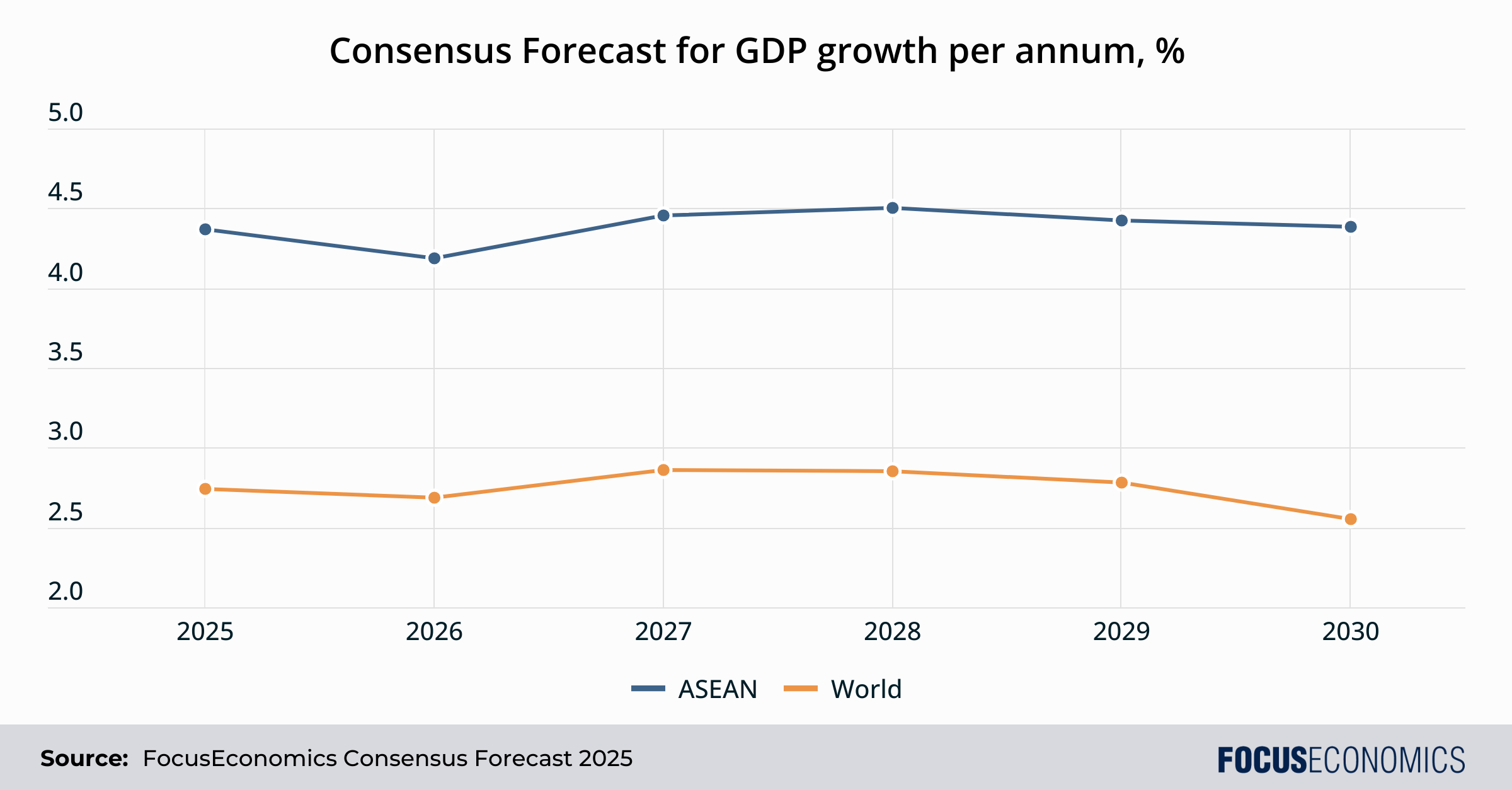

The Consensus among our panelists is relatively upbeat. ASEAN’s GDP growth is seen averaging 4.4% between now and 2030, with Cambodia, Indonesia, the Philippines and Vietnam the top performers. Among world regions, only South Asia is expected to perform better—chiefly as a result of India’s economic rise.

That said, the region will have to battle an unenviable list of challenges—a more closed-off U.S., Chinese manufacturing dominance, AI stealing services jobs, increasingly common extreme weather events as the climate warms, and political disaffection among the young. As a result, Southeast Asia could end up being a key case study as to whether the old path to prosperity is alive and well—or if indeed such a path still exists.