If you let yourself be guided solely by the tariff threats coming out of Washington over the past year, you might assume Asia’s export engines were sputtering, choked by the fumes of a renewed trade war. You would be wrong. As the dust settles on 2025, the numbers tell a different story: One of a boom that has more than outweighed the impact of tariffs. This has surprised analysts, many of whom initially saw U.S. levies giving Asia’s economy a knock.

Why the AI boom is boosting Asia’s export performance

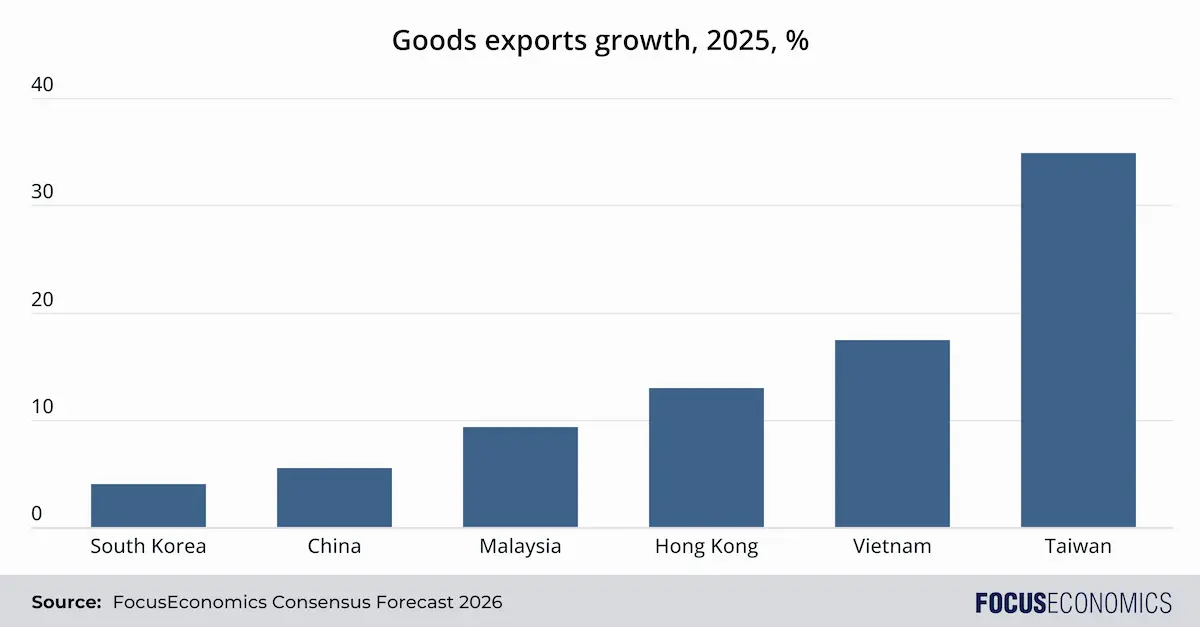

To understand the current mood in Asia’s trade ministries, look at the scoreboard. Taiwan’s exports surged nearly 35% in 2025, obliterating previous records. South Korea saw its outbound shipments crack the USD 700bn ceiling for the first time. China’s trade surplus surged to a record high despite being singled out by U.S. President Trump for country-specific tariffs. Overall, Asia’s goods exports rose at the fastest rate since 2022, when sales were boosted by remote working and strong consumer spending post-lockdown. In short, amidst all the geopolitical volatility, the aggregate data for the “Factory of Asia” is flashing a defiant green.

Two opposing forces are colliding. On one side is the “Trump Shock”—the broad U.S. tariffs enacted last year which were designed to onshore American manufacturing and punish trade imbalances. On the other is the “AI Lift”—an insatiable, price-insensitive global hunger for the computing power required to train and run generative artificial intelligence models. American hyperscalers—Microsoft, Amazon, Google—are investing hundreds of billions of dollars to build data centers that consume large quantities of silicon. For now, the lift is winning. The sheer velocity of the tech cycle has overwhelmed the friction of trade policy; anything involving a logic gate or a memory cell is flying off the shelves. Moreover, semiconductors—the backbone of the electronics industry—were explicitly exempt from U.S. tariffs anyway.

Asia, with its dominance in much of the electronics supply chain, has thus benefited as a result; in 2025 the region contributed nearly two-thirds of the growth in global AI-related trade. South Korea and Taiwan focus on fabricating the most advanced chips, while Japanese firms are important suppliers of chip equipment and machinery. China dominates in mid-level manufacturing and assembly, areas where other countries like India, Malaysia, Vietnam and Thailand are also present.

The semiconductor cycle explained: Why it matters for exports

The semiconductor industry moves in peaks and troughs, with the bust of 2023–2024 quickly giving way to the current upswing. The mechanics of this recovery are crucial. During the post-pandemic hangover, the world was awash in memory chips. Prices for DRAM (Dynamic Random Access Memory) and NAND (storage) collapsed. But in late 2024, the inventory cleared. Then came the AI twist. AI servers do not just need more memory; they need better memory. Concretely, they require High Bandwidth Memory (HBM), a complex 3D-stacked architecture that commands a premium over standard chips.

This has created a “super-cycle” for price recovery. Because HBM is difficult to manufacture, it eats up production capacity, creating a shortage of standard chips for PCs and phones. The result? Prices rise across the board. However, if the past is anything to go by, the current upswing will be followed in the not-too-distant future by price declines as new chip factories currently in the pipeline come on stream and supply rises as a result.

Taiwan semiconductor exports: The epicenter of the boom

Taiwan’s export performance in 2025 was nothing short of defying gravity. Exports of Information and Communication Technology (ICT) products soared nearly 90%, with the country’s trade surplus doubling to a staggering USD 157bn. The sales boom has been driven by higher sales to the U.S., with the country overtaking China as Taiwan’s largest export market for the first time in decades.

At the heart of this is TSMC (Taiwan Semiconductor Manufacturing Company). The foundry’s near-monopoly on the sub-5-nanometer chips that power the most advanced AI means that Taiwan is effectively exporting the world’s most valuable resource: compute. The company is ramping up capital expenditure to meet surging global demand: Investment of over USD 50 billion is planned for this year, up from an already-high USD 40 billion in 2025.

Are Trump’s tariffs affecting Asian exports?

The boom in global AI demand has masked the impact of U.S. tariffs which—though not applying to semiconductors last year—were levied on other Asian exports. Large-scale trade destruction due to tariffs is not yet evident; if anything exports were boosted in the first half of 2025 by firms front-loading sales ahead of threatened levies.

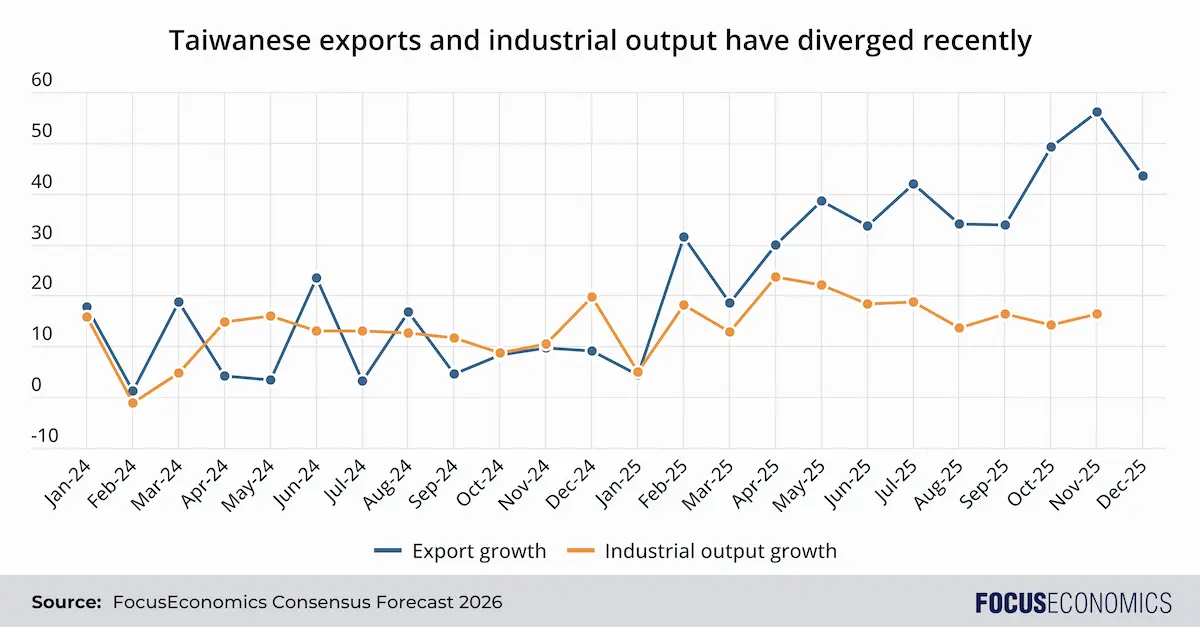

However, trade diversion is very much present. Specifically, direct Chinese exports to the U.S. collapsed from USD 439 billion in 2024 to USD 266 billion in 2025. At the same time, Chinese sales to other Asian markets, emerging markets more generally plus the EU surged. Part of this was due to Chinese firms gaining genuine market share outside the U.S., but some goods seem to have been rerouted via third countries on their way to the U.S. For instance, Taiwanese export growth has typically tracked domestic industrial production fairly well. However, 2025 saw a large discrepancy suddenly emerge, with exports racing far ahead of industrial output; this suggests at least some exports were Chinese transshipments.

The key factor that could change this dynamic going forward is future U.S. tariffs on foreign semiconductors. Trump introduced limited levies of 25% on certain types of chips in January 2026; a broader import tax on semiconductors could bring Asia’s export party to a halt.

Export forecasts: What our panelists expect for Asia in 2026

Our Consensus Forecast is currently for Asian goods export growth to slow sharply in 2026 to just above 1%, as front-loading to the U.S. is exhausted. However, given the region’s better-than-expected export performance last year and that a major semiconductor organization recently projected semiconductor sales would rise another 26% in 2026, risks to our panelists’ forecasts appear skewed to the upside and could well be revised up going forward.

The key risk is without doubt a broad-based U.S. chip tariff. However, this appears unlikely at present given the U.S. cannot easily make such chips domestically in the short term; semiconductor factories have long lead times. Increased EU trade restrictions on China are a further factor to watch. A Chinese attack on Taiwan, while a tail risk, could do major damage to global supply of the most advanced electronics.

Insight from our panelists

On the 2026 outlook, EIU analysts said:

“The front-loading of global exports orders that benefited growth in 2025 will flip to a headwind, as there is a period of “payback” for demand that was brought forward. That will occur amid slowing US and global growth as the economic impact of rising tariffs builds. Artificial intelligence investment-related demand for semiconductors and electrical and energy equipment will put a floor under regional trade, but presents some risks if the spending boom slows.”

Nomura analysts said:

“The boom in US AI capex is translating into increased export orders in Asia for specialty materials, advanced and memory chips, advanced packaging, assembly and testing, semiconductor equipment, and precision machinery. While the intellectual property for AI is largely US-based, much of the physical production takes place in Asia, benefitting the region through the semiconductor value chain. Rising AI demand is also lifting capex within Asia. Foundries are expanding advanced node and advanced packaging capacity; memory firms are expanding high-end lines, and server manufacturers are investing in new assembly and testing facilities across the region. There is also an increase in third-party data centers in Asia, which is boosting demand for electrical equipment, cooling systems and other infrastructure such as power and land.”

On China, Goldman Sachs analysts said:

“China’s exports were resilient in 2025 despite higher US tariffs, with real inflation-adjusted growth in exports on track to reach around 8% for the full year. That’s partly due to a robust increase in exports to emerging market economies. Meanwhile, falling export prices are making Chinese products increasingly competitive. The expected resilience of Chinese exports this year is linked to three factors, according to Shan [Goldman Sachs’ chief China economist]: the rapid expansion of exports to emerging market economies, limited ability for other countries to impose significant trade barriers against China in the face of its dominance in critical minerals, and the potential for greater growth in high-tech exports.”