Biggest Global Economies

According to our Consensus Forecast, of the top 10 largest economies in 2026, five will be in Europe, three in Asia and two in the Americas. Most of these economies—concretely the G7 members—are already wealthy in USD GDP per capita terms. However, there are also a few emerging markets on the list that are still relatively poor in per-person terms and whose large economic size is linked instead to their huge domestic populations. Likewise, while most of the economies in the top 10 have potential growth rates below the global average due to already high physical and human capital stocks, two of the Asian economies listed buck that trend.

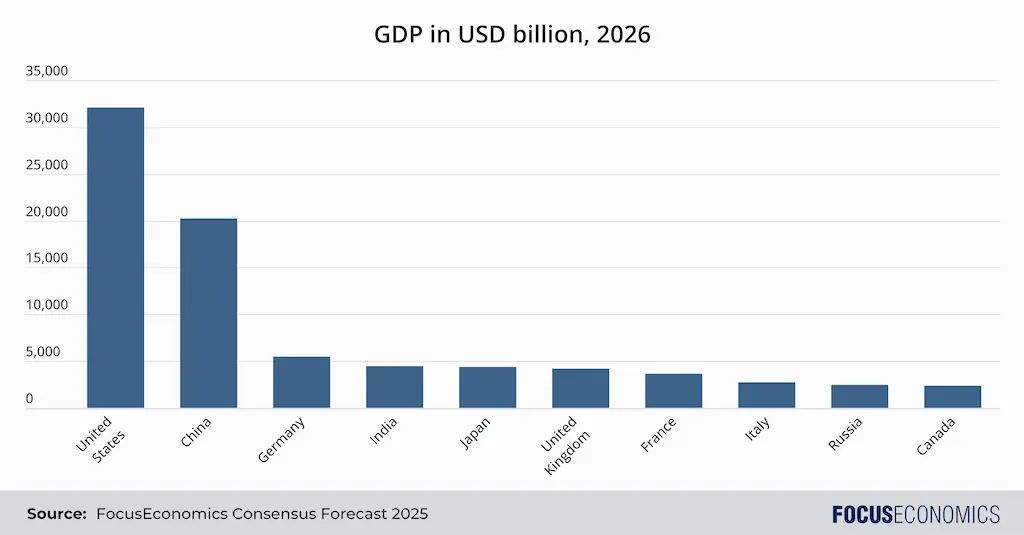

Top 5 Economies in the World

1. United States

2026 GDP: USD 32.1 trillion

The United States’ GDP is the world’s largest, being worth over a quarter of global output in nominal GDP terms. Moreover, it has among the world’s highest GDP per capita. The economy’s structure is highly diversified. The tech industry, anchored by Silicon Valley, dominates globally, driving innovation in AI, biotech and software. The financial sector, centered in New York, boasts the world’s deepest capital markets. Healthcare and pharmaceuticals are other strengths, while manufacturing—though reduced in scale compared to previous decades—remains competitive in areas such as aerospace, defense and motor vehicles.

Since the Covid-19 pandemic, the gap between the U.S. and other major advanced economies has widened due to a pickup in productivity growth, relatively robust private spending and the country’s AI boom. This outperformance is set to continue going forward: Our Consensus Forecast is for economic growth of around 2% per year for the rest of this decade, compared to 1.4% for the Euro area and less than 1% in Japan.

That said, the economy faces challenges, including the highest income inequality in the G7, aging infrastructure, high healthcare costs and mounting national debt. Regarding the latter, the U.S. will likely continue to run a budget deficit far wider than other advanced economies, causing public debt to continue to rise as a share of total output in the coming years. Moreover, the economy is vulnerable to a pullback in frothy stock market values and AI spending—two factors that have driven private consumption and fixed investment respectively over the last year.

2. China

2026 GDP: USD 20.2 trillion

China’s GDP is the world’s second largest, being worth close to 20% of global GDP in nominal USD. It is powered by investment and export-led manufacturing; private consumption is still around 20 percentage points of GDP lower than in developed economies. Known as the “world’s factory,” China is the leading producer of electronics, machinery and textiles. The government has recently prioritized technological self-reliance and increased value-added activities, showering domestic industries with subsidies and state support and restricting the participation of foreign firms in sensitive areas of the economy. This has led to some impressive results, including the emergence of highly competitive local juggernauts such as Huawei and Tencent in the tech space and BYD in electric vehicles. In recent years, such firms have increasingly broken into overseas markets, causing alarm in the West. Government support has also helped make China’s economy a leader in the green space: Chinese firms produce the majority of the world’s solar panels for instance.

Relative to the U.S. economy, China has lost pace since 2021 due to the depreciation of the yuan versus the dollar coupled with robust economic activity in the U.S. Our analysts’ estimates are for convergence to resume over our forecast horizon, but at a slower pace than in the past as China’s potential growth ebbs.

China faces multiple challenges, including high levels of corporate debt, dealing with the demands of a declining and aging population, a weak property market, and geopolitical tensions with the West—with the latter set to be a frequent feature of President Trump’s second term.

3. Germany

2026 GDP: USD 5.4 trillion

Germany is Europe’s largest economy. Though services is the main economic sector, Germany also has a strong industrial base; the manufacturing sector is around twice as big as that of other G7 economies as a share of GDP. The Mittelstand—a dense web of medium-sized industrial enterprises—forms the backbone of this. The country benefits from a skilled workforce, prudent fiscal management and a favorable geographical position at the heart of Europe.

That said, the country’s export-oriented, manufacturing-heavy economic model has come under threat in recent years from rising global trade tensions, the country’s struggle to adapt to new forms of technology, and the increasing competitiveness of Chinese firms—particularly in the automotive space. Volkswagen’s announcement in 2024 that it intended to close several factories is indicative of the latter. An aging population, dependence on imported fossil fuels and political fragmentation amid the rise of the right-wing AfD party are additional challenges. Since 2018, Germany’s GDP growth has lagged well below the G7 average. Despite the announcement of a EUR 500 billion stimulus package, this trend will likely continue in the coming years.

4. India

2026 GDP: USD 4.5 trillion

India’s GDP is growing fast, having more than doubled in size over the last decade. Unlike many other Asian economies, India does not have a huge manufacturing sector, notwithstanding the government’s recent Make In India initiative. Rather, services output drives GDP. India boasts particular strength in IT; collectively, the country’s two IT giants, Infosys and TCS, employ around a million people. The pharmaceutical industry is another strong suit, especially in the field of generic drugs. However, the agricultural sector, which employs a large portion of the population and still accounts for around a fifth of the economy, remains less productive and vulnerable to climate risks.

India’s economy has a number of strengths, including a fast-growing and entrepreneurial population, a highly educated English-speaking workforce, a vast domestic market and political stability. That said, infrastructure gaps—particularly in rural areas—are a roadblock. Additionally, regulatory challenges and bureaucratic hurdles pose difficulties for businesses, and the country is still not able to guarantee quality universal education. Tensions with the U.S. are an additional problem; Donald Trump imposed hefty tariffs on India in 2025 for its continued purchases of Russian oil.

Our Consensus is for the economy to remain among Asia’s fastest-growing in the coming years, but growth could be significantly faster with the right reforms; at below 7% per year, India’s growth forecasts for the coming years are still significantly below the pace that China was growing at when it had a similar GDP per capita.

5. Japan

2026 GDP: USD 4.4 trillion

Japan’s economy, while still the fifth largest in the world, has waned in relevance since the 1990s, at which point it was the second-largest economy and closing in on the U.S. in top spot. Like Germany, Japan has a large manufacturing sector worth close to 20% of GDP, with strengths in electronics, motor vehicles and robotics; Japanese companies like Mitsubishi, Sony and Toyota play leading roles globally. Japan also has a significant banking and financial services sector. The economy is export-oriented, and has persistently registered trade and current account surpluses in recent years.

However, Japan faces significant demographic challenges, including a rapidly aging population and low birth rates that drag on GDP despite persistent fiscal stimulus. Dependence on imported energy and raw materials is another weakness, as it makes the economy vulnerable to global price shifts. Our panelists forecast Japan’s GDP growth to average below 1% for the remainder of this decade, and to record the joint-weakest performance in the G7 along with Italy.

Economies 6-10

6. United Kingdom

2026 GDP: USD 4.2 trillion

The UK economy is predominantly service-oriented, with insurance, finance and real estate as key contributors—particularly through the City of London, a major global financial hub. Other key sectors include creative industries, defense, higher education, motor vehicles and pharmaceuticals. A flexible labor market and well-performing education system are key strengths.

However, Brexit has introduced challenges, particularly for trade and labor mobility with the EU: This, in turn, has hampered exports and investment since the UK left the bloc. While the UK could strike some sector-by-sector deals with the EU in the coming years, economic ties with the bloc are unlikely to grow substantially closer in the medium term. Additionally, the authorities face the difficulty of satisfying rising public spending demands in a low GDP growth environment, all without spooking markets by issuing lots of new debt. The Labour government that took office in 2024 has increased spending and taxes in a bid to tackle this situation, but the budget deficit is expected to remain wide at over 3% of GDP in the coming years.

Our analysts’ forecasts for the coming years are for UK GDP growth to be around half a percentage point per year lower than in the decade leading up to the Covid-19 pandemic, due to the lasting knock caused by Brexit.

7. France

2026 GDP: USD 3.6 trillion

France’s economy is highly diversified. The country is a leading global exporter of luxury brands like Chanel, Hermès and LVMH. Aerospace, led by Airbus, is also a crucial sector. France’s agricultural sector is the largest in the EU, and is known for dairy, grain and wine production. Moreover, since Brexit, Paris has increased its status as a financial center; the European Banking Authority relocated to Paris, and the capital has created thousands of new financial-service jobs.

The state has a strong role in the economy. Government spending is close to 60% of GDP, much higher than in most European neighbors. Moreover, the state owns shares in many large companies, such as nuclear power producer EDF, airplane manufacturer Airbus, and car maker Renault. This sizable state footprint has in recent years translated into some of the widest fiscal deficits in the EU, in turn causing French borrowing costs to exceed those of Greece and Spain.

France’s GDP growth in the coming years will be below the EU average. Political instability and the need to rein in the fiscal deficit will act as a drag, while frequent public protests will likely continue to pose a challenge to policymakers.

8. Italy

2026 GDP: USD 2.7 trillion

Italy’s GDP is dominated by services, but also has manufacturing strengths in luxury goods, machinery and motor vehicles. Northern Italy, home to industrial hubs like Milan and brands like Fiat and Ferrari, drives much of this manufacturing activity. Italy is also Europe’s third-largest agricultural producer, famous for wine and olive oil.

In recent decades, political instability, a high public debt-to-GDP ratio, a sclerotic public sector, deteriorating demographics and large regional disparities between the industrialized north and underdeveloped south have posed challenges. Though the economy is currently receiving a sizable boost from the disbursement of EU recovery funds, annual GDP growth is unlikely to top 1% this year or in the years that follow. As such, Italy’s economic heft will continue to ebb going forward.

9. Russia

2026 GDP: USD 2.5 trillion

Russia’s economy depends on natural resources, with oil and natural gas making up over half of its export revenues and state-controlled giants like Gazprom and Rosneft dominating energy production. This energy reliance has spurred significant economic growth but also makes Russia vulnerable to global price fluctuations and energy sanctions. The manufacturing sector is centered on heavy industries, including arms, chemicals and steel; moreover, Russia is one of the world’s largest grain exporters. Since the invasion of Ukraine in 2022, Russia’s economy has become more dependent on the military sector and government spending, and more reliant on Asia at the expense of Europe.

The economy has been much more robust than more analysts expected since the Ukraine war broke out, with Russia’s GDP growth above 3% in 2023 and 2024, thanks to higher military spending, social handouts and the government’s ability to circumvent sanctions. That said, economic momentum slowed sharply in 2025 amid lower oil prices, tighter sanctions, Ukrainian damage to energy infrastructure and the exhaustion of the war-related spending boost. Economic growth is forecast to pick up to around 1.5% in the medium term according to our panelists’ estimates, likely on the assumption that an eventual end to the conflict in Ukraine will provide a boost to labor supply, investment and exports.

10. Canada

2026 GDP: USD 2.4 trillion

Canada’s economy is resource-rich, with oil, forestry and mining making an important contribution to exports. That said, Canada’s GDP as a whole is still dominated by the services sector, with financial and tech services particular strengths. In recent years economic activity has been buoyed by strong demand in key trading partner the U.S., as well as by a rapid rise in the population—from 2019 to 2024 the population rose around 10%, above the historical trend. That said, the government recently cut immigration quotas in the face of rising unemployment and public dissatisfaction over high housing costs. As a result, population growth in 2025 should almost grind to a halt from around 3% in 2024. Moreover, the U.S. hit Canada with tariffs in 2025, curbing Canadian exports.

Despite its large natural resources, skilled workforce and clean governance, Canada faces vulnerabilities including fluctuating prices for its commodity exports, high household debt and trade dependency on the U.S. The latter could be a particular risk in 2026 due to the scheduled renewal of the USMCA trade deal with Mexico and the U.S; Donald Trump is likely to push for a deal more favorable to American interests.

Factors Influencing GDP Rankings in 2026

A nation’s economy is the combination of its output per person multiplied by the population size. As such, countries with large populations (such as China and India) tend to have higher total GDP than those with smaller populations, even if they are less wealthy in per capita terms. Moreover, output per person is determined by myriad factors, such as the quality of health and education, physical infrastructure, ease of doing business, corruption, natural resource endowment, etc.

Future Projections for the World’s Biggest Economies

The list of the top 10 largest economies in the world is likely to grow more diverse in the coming decades. The number of G7 economies featured will decline, while emerging markets such as Brazil, Indonesia and Mexico could join the top tier given their large populations and ample potential for catch-up growth with the West. Moreover, China and India will continue to gain relative economic clout. For instance, the long-term projections of the economists that we poll show that by 2033, India will have become the world’s third-largest economy, while China’s GDP will be around USD 24 trillion larger than Germany’s, compared to around USD 14 trillion bigger today.

Insight from our expert analysts

On risks to the U.S. outlook, analysts at the EIU said:

“A sharp tech or AI-related stockmarket bust would rank among the most serious downside risks to the US growth outlook. A large, sustained equity correction of dot-com magnitude today would lower the level of US GDP as higher risk premia, weaker business investment and tighter credit conditions feed through the economy. The shock is likely to be larger than the dot-com period because US households are now far more exposed to equity prices: direct and mutual-fund equity holdings account for a much larger share of household assets than in 2000, so a market slump would generate powerful negative wealth effects and a marked slowdown in consumption. At the same time, AI-related projects currently account for more than the entirety of US business fixed investment growth, meaning that a sudden reassessment of AI earnings prospects would trigger a disproportionate pull-back in capital expenditure and hiring.”

On China, Nomura analysts commented:

“We expect GDP growth to slow further to 4.1% in Q1 2026 from 4.3% in Q4 2025 due to the rising payback effect of the trade-in program and worsening sentiment in the property sector. By spring 2026, the slowdown will likely have become painful enough to push Beijing to step up stimulus to arrest the slowdown. To effectively cope with these mounting challenges, we believe Beijing needs to take bolder actions to clean up the mess in the property sector, support consumption in a more sustainable way by reforming the pension system, fix the fiscal system to better protect business owners and improve its trade relationships with other economies.”

If you enjoyed this article, why not check out our blog post on the world’s top 10 poorest economies?

Originally published in December 2017, updated in December 2025