In our latest special report, we take a deep dive into our panelists’ outlook for emerging economies next year, looking at GDP forecasts for entire regions and individual countries plus key trends, drivers and risks. Below is a snapshot of those projections.

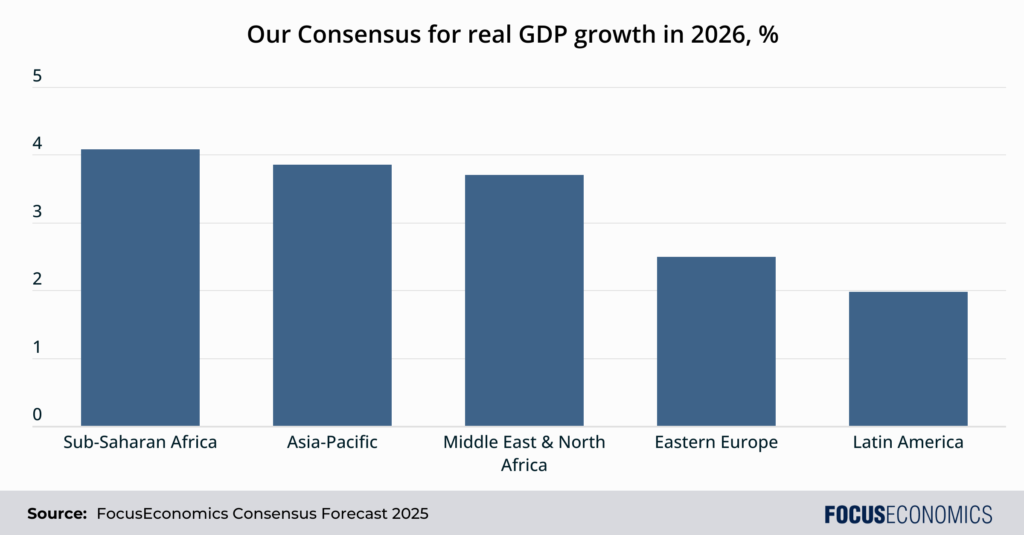

Asia-Pacific: As has been the case in recent decades, Asia-Pacific will be among the fastest-growing regional economies in 2026. Supportive factors include tourism, the region’s strong presence in dynamic sectors such as IT and electronics, business-friendly policymaking, high educational standards compared to many other emerging markets, and still-solid population growth.

Latin America: Latin America is forecast to be the slowest-growing emerging market region in 2026. This is partly a consequence of relatively high GDP per capita—Latin America is full of middle and high-income countries according to the World Bank’s definition—leaving less space for easy catch-up growth. In addition, the region will be held back by political instability, underperforming education systems, corruption, violence and a lack of presence in high-growth sectors.

Sub-Saharan Africa: Sub-Saharan Africa (SSA) should pip Asia-Pacific as the world’s fastest growing region next year with a 4.1% rise, a trend expected to continue over our forecast horizon. A key factor supporting SSA is the quickest rate of population expansion anywhere in the world—next year, this expansion is predicted at 2.4% in annual terms. As such, regional output per head is only forecast to rise at a modest pace in 2026.

The Middle East and North Africa: The Middle East and North Africa (MENA) economy should expand at the fastest pace since the pandemic recovery next year. Higher OPEC oil production quotas will be a key factor supporting the economic outlook next year. Though the cartel recently paused output increases in Q1 2026, permitted production levels over 2026 as a whole should still be markedly above 2025 levels.

Eastern Europe and Central Asia: Eastern Europe and Central Asia is projected by our panelists to be the second-slowest emerging-market region in 2026. As with Latin America, this is partly because many Eastern European economies—chiefly those within the EU—are converging or have converged with developed-economy levels of GDP per capita, leaving less room for catch-up growth. Softer crude and gas prices compared to 2025 could be a further drag by constraining government spending in energy exporters.

Insight from our panelists:

On the Latin American outlook, EIU analysts said:

“The fallout from US protectionism—including the uncertainty this is creating—will dampen trade and investment in Latin America. Mexico’s economy will be hit the hardest, given its close ties with the US, whereas the impact on Brazil and other South American commodity exporters will be partially offset by their greater trade relationships with China. A rebound in Argentina’s economy from a two-year slump that ran into headwinds in the third quarter should now resume following US financial assistance and gains in Congress at the mid-term legislative elections in October for the ruling party of the president, Javier Milei. Opportunities in Latin America in critical minerals, energy and infrastructure will remain attractive for investors.”

On the impact of U.S. tariffs on Asia’s economy, Nomura analysts said:

“With reciprocal tariffs having risen from 10% in July to 15-20% in August, further margin compression is likely in the months ahead. Temporary measures such as cost cutting and running down inventories to delay a price increase in the US will not be sustainable in the long run. This is consistent with what we have observed in Q2 corporate earnings, where firms warned of further margin hits as cost-saving measures reach their limits. Higher US tariffs have left Asian exporters with a difficult choice: either pass on the rising costs and put US market share at risk, or absorb the costs and take the hit in profitability. This has been aggravated by local currency appreciation and competitive price pressures. Economies with higher-value, brand-driven exports tend to hold prices steady for longer, sacrificing margins, whereas low-margin exporters make a quicker move to pass on costs, risking competitiveness.”

Our latest analysis:

- Israel’s economy massively beat market expectations in Q3.

- In contrast, the UK economy lost steam in Q3.

Event Partnerships:

We are proud to support a diverse range of industry events that bring together leaders, innovators, and decision-makers from around the world.

Special discounts for FocusEconomics members!

Join industry experts in Toronto for a key event focused on strengthening model risk governance, addressing AI-driven challenges, and navigating evolving regulations like OSFI’s E-23. This conference will provide practical insights on how institutions can manage complex models and expand oversight while optimizing resources.

Topics Include:

-

Navigating OSFI’s E-23 and AI/ML integration

-

Strengthening model documentation and vendor oversight

-

AI governance and fairness in generative models

-

Overcoming challenges in model validation with limited resources

-

Accelerating AI-driven AML innovation with oversigh