Africa’s economic narrative has mutated considerably in recent decades. At the turn of the millennium, The Economist infamously branded it “The Hopeless Continent,” a place seemingly condemned to perpetual war, famine, and poverty. A decade later, the narrative had flipped to “Africa Rising,” buoyed by a commodities supercycle and the promise of a demographic dividend. Today, the mood is more somber, settled in a realism that acknowledges a stark divergence: while some nations are sprinting toward middle-income status, others are mired in a sclerotic trap of debt and dysfunction.

Africa remains the poorest continent on Earth, a reality that is not merely a statistical artifact but a human tragedy. It is home to 18% of the world’s population but accounts for less than 3% of global GDP. The question of why is the most pressing inquiry in development economics. The answer is not singular; it is a complex interplay of geography, history, and institutional failure, all compounded by modern policy choices. To understand Africa’s poverty is to understand a continent of fifty-four distinct national experiments, some succeeding against the odds, others failing despite immense natural wealth.

Economic Factors Making Africa the Poorest Continent

The genesis of African poverty is often debated through two primary lenses: geography and institutions. The “geography hypothesis,” championed by scholars like Jeffrey Sachs, posits that Africa has been dealt a terrible hand. A vast proportion of the continent lies within the tropics, creating a breeding ground for diseases like malaria and schistosomiasis, which historically decimated human capital and stifled productivity. Unlike Europe or North America, Africa lacks a dense network of navigable rivers—the natural highways of pre-industrial trade. The continent’s coastline is remarkably smooth, lacking the deep natural harbors that facilitated the rise of trading empires in the West and East. Furthermore, a significant number of African nations are landlocked, forcing them to rely on their neighbors’ often crumbling infrastructure to access global markets, essentially imposing a heavy tax on every container of goods exported.

However, geography is destiny only if institutions fail to overcome it. The “institutions hypothesis,” articulated by economists such as Acemoglu and Robinson, argues that the root cause is political. For centuries, Africa has been plagued by “extractive institutions”—systems designed to loot Africa’s natural resources for a narrow elite rather than create wealth for the broad population. This legacy, sharpened by the transatlantic slave trade and calcified by colonialism, created economies structured for extraction, not production. Colonial powers built railways not to connect African cities to one another, but to connect mines to ports. When independence arrived, many post-colonial leaders, rather than dismantling these systems, simply took over the controls.

This institutional weakness manifests most acutely in the “Resource Curse.” It is a cruel paradox that the poorest Africans often live on the richest land. Countries like the Democratic Republic of Congo (DRC) and Equatorial Guinea sit atop trillions of dollars in minerals and oil, yet their populations languish in penury. The influx of resource rents inflates the currency (Dutch Disease), rendering other sectors like agriculture and manufacturing uncompetitive. Worse, it detaches the government from the citizen. When a state derives its revenue from a hole in the ground rather than from taxing its people, it has no incentive to build the schools, roads, or legal systems that taxpayers demand. The social contract is broken before it is even signed.

Africa’s infrastructure development—or the lack thereof—is the physical manifestation of these failures. The World Bank estimates that the infrastructure gap reduces business productivity in Africa by 40%. The energy deficit is particularly crippling; over 600 million Africans lack access to electricity. Manufacturing, the traditional escalator out of poverty, is impossible when the power grid is erratic and electricity costs are three times the global average. Consequently, Africa has largely deindustrialized prematurely, shifting from subsistence agriculture directly to low-productivity informal services, bypassing the factory jobs that built the middle class in Asia.

Finally, the fragmentation of African markets creates a ceiling on growth. The continent is a patchwork of small, disconnected economies. Intra-African trade stands at a paltry 16%, compared to nearly 60% in Asia and 70% in Europe. Borders are thick with red tape and tariffs, meaning it is often cheaper for a Ghanaian business to trade with Portugal than with Nigeria. This balkanization prevents companies from achieving economies of scale, keeping African firms small, uncompetitive, and vulnerable to global shocks.

Solutions to These Problems

The path out of this labyrinth and to greater development is neither secret nor magical; it requires the grinding, unglamorous work of structural reform. The first and most critical solution is the demolition of barriers to trade. The African Continental Free Trade Area (AfCFTA) signed in 2018 is the continent’s “Marshall Plan.” By creating the world’s largest single market by number of countries, it aims to boost intra-African trade by 52% by eliminating tariffs on 90% of goods. If fully implemented, the AfCFTA will allow an Ethiopian textile manufacturer to sell duty-free to South Africa, hopefully creating the economies of scale necessary to compete with Asian giants. But treaties signed in Kigali mean nothing if trucks are stuck at the border in Beitbridge. Hard infrastructure—roads, rails, and ports—must accompany soft infrastructure: digital customs, harmonized standards, and visa-free travel for business.

Second, the “Resource Curse” must be broken through diversification plus the development of mineral processing and refinement. For instance, countries like Ghana and Cote d’Ivoire, which produce 60% of the world’s cocoa yet capture less than 6% of the chocolate market’s value, are finally moving to process beans locally. In the mining sector, nations like Tanzania and Zimbabwe are banning the export of raw lithium, demanding that battery processing happen on African soil. This shift from extraction to industrialization creates jobs and transfers technology.

Third, the energy deficit must be solved not just by plugging into the grid, but by redefining it. While mega-projects like the Grand Ethiopian Renaissance Dam are vital, the immediate solution for rural Africa lies in decentralized renewable energy. Off-grid solar and mini-grids are doing for electricity what mobile phones did for telecommunications: leapfrogging the need for expensive, centralized infrastructure. This empowers the small-scale entrepreneur—the welder in Lagos or the miller in rural Kenya—who is the true engine of African growth.

Finally, governance must pivot from patronage to performance. The “Singapore Model”—authoritarian efficiency—has found fans in Rwanda, but the broader solution is the strengthening of independent institutions: courts that enforce contracts, central banks that tame inflation, and anti-corruption bodies that actually bite. Digitalization is a powerful disinfectant here. Moving government procurement and tax collection online, as Kenya has done, reduces the surface area for bribery and increases state revenue.

Africa’s Economic Performance Since the Turn of This Century

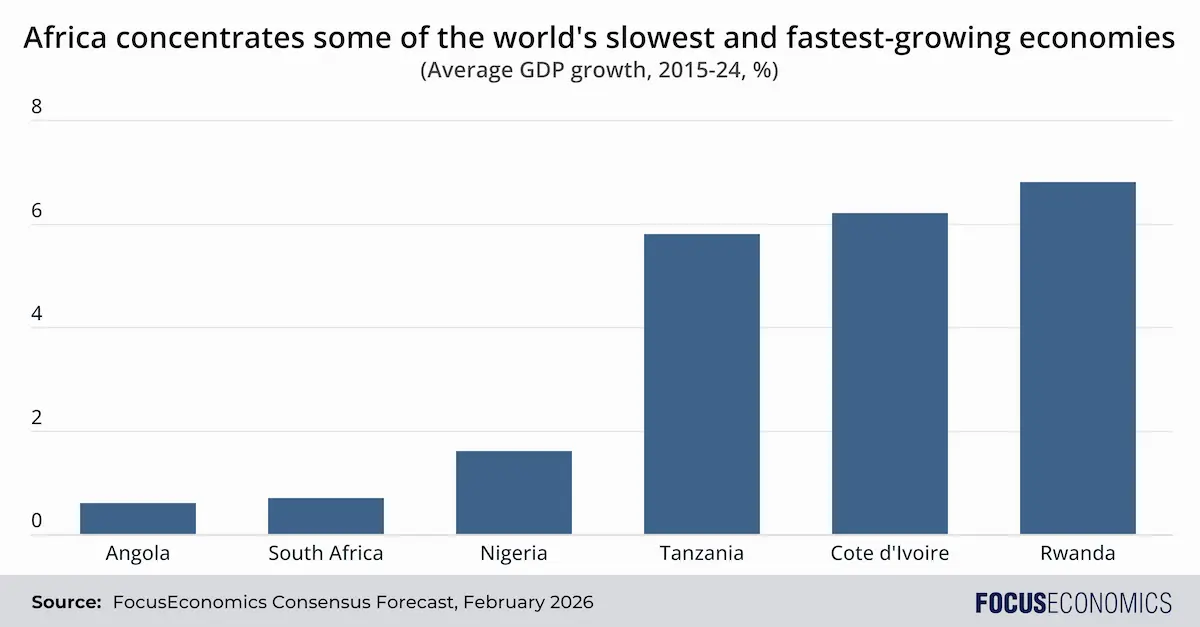

The economic history of Africa since 2000 is a tale of two trajectories: the “Lions” and the “Petro-states.” The period from 2000 to 2014 was the golden age of “Africa Rising,” driven largely by China’s insatiable appetite for commodities. GDP growth across the continent averaged 5% annually, outpacing the global average. However, when the commodity supercycle crashed in 2014, the tide went out, revealing which economies had built solid foundations and which were merely floating on oil.

The Best Performers: The true success stories of the 21st century are the non-resource-intensive economies that focused on governance, diversification, and strengthening the investment climate.

- Ethiopia: Once the poster child for famine, Ethiopia has engineered an economic miracle, averaging nearly 10% GDP growth so far this century. Following a state-led development model similar to China’s, the government poured billions into infrastructure—dams, railways, and industrial parks. While recent conflict in Tigray has tarnished this progress, the country’s transformation remains a testament to the power of industrial policy.

- Rwanda: Rising from the ashes of the 1994 genocide, Rwanda has branded itself as the “Singapore of Africa.” President Paul Kagame’s regime, though politically authoritarian, has been economically liberal and hyper-efficient. By slashing corruption and digitizing government services, Rwanda has consistently ranked as one of the easiest places to do business on the continent, maintaining high growth rates and dramatically improving human development indicators.

- Mauritius and Seychelles: These two island nations have graduated to upper-middle and high-income status respectively, proving that geography need not be a prison. Through prudent management of tourism, offshore finance, and fisheries, they have achieved standards of living comparable to parts of Europe, with strong social safety nets and stable democracies.

- Cote d’Ivoire (Ivory Coast): Since emerging from civil war in 2011, Cote d’Ivoire has been a star performer in West Africa, averaging 7% growth. It has diversified beyond cocoa, investing heavily in energy and transport infrastructure, becoming a magnet for francophone investment.

The Worst Performers: Conversely, the laggards are almost exclusively countries that failed to diversify away from commodities or imploded due to governance failures.

- Zimbabwe: Under Robert Mugabe and his successors, Zimbabwe offered a masterclass in economic destruction. Hyperinflation, the violent seizure of commercial farms, and the abandonment of the rule of law turned the “breadbasket of Africa” into a basket case. The economy has contracted sharply multiple times, and the currency has collapsed repeatedly, wiping out the savings of generations.

- Equatorial Guinea: Despite having one of the highest GDPs per capita in Africa on paper due to oil wealth, the reality on the ground is dystopian. The wealth is almost entirely concentrated in the hands of the ruling elite, while health and education indicators rival those of the poorest nations on earth. As oil production has declined in recent years the economy has shrunk in tandem.

- South Africa: South Africa—the continent’s most industrialized economy and among its wealthiest in per person terms—has endured a “lost decade” of stagnation. Crippled by “state capture” (systemic corruption), a collapsed energy utility (Eskom) that has subjected the country to daily blackouts, and rigid labor markets, growth has averaged less than 1% in recent years—far below the rate of population growth, leading to rising per capita poverty.

- The Democratic Republic of Congo (DRC): Despite holding mineral wealth estimated at $24 trillion, the DRC remains one of the poorest places in the world. Decades of conflict, weak state authority, and foreign meddling have made its resources a curse rather than a blessing, fueling armed groups rather than the national budget. Most recently, the DRC has faced an insurgency by the Rwanda-backed M23 group in the east of the country, with the conflict lingering despite a U.S.-brokered ceasefire.

Africa’s Economic Outlook

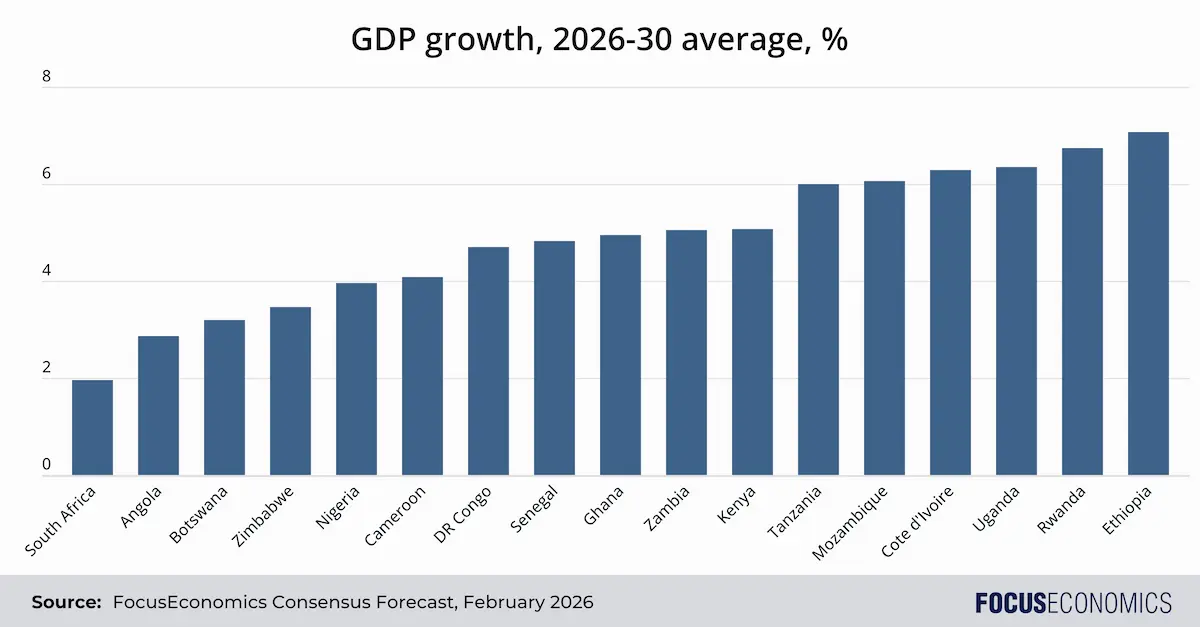

On aggregate, our Consensus is for Sub-Saharan African GDP to rise 4.2% out to 2030. This will make the region the world’s fastest growing, ahead of the Asia-Pacific, though the overall figure masks huge discrepancies between countries.

The Bright Spots: The continent’s economic center of gravity is shifting, with East Africa and parts of West Africa to lead the continent’s growth in the coming years. Examples of economies our panelists expect to perform particularly well are:

- Senegal: With major oil and gas fields coming online, combined with a relatively stable democracy and the “Plan Senegal Emergent,” the country is projected to see double-digit growth in the short term and sustained high growth thereafter.

- Rwanda: The Rwandan economy is set to continue its remarkable rise in coming years, buoyed by the government’s concerted plans, including a new airport which aims to position the country as a continental travel hub.

- Kenya: As the tech hub of the continent (“Silicon Savannah”), Kenya is positioning itself as a leader in services, finance, and renewable energy. Its diversified economy makes it resilient, although debt remains a concern.

- Cote d’Ivoire: Already the world’s cocoa superpower, the Ivorian economy has recently found a new gear with the massive Baleine oil and gas field coming online. This energy windfall, supported by infrastructure development and the National Development Plan’s focus on industrial processing, should underpin strong GDP growth in the coming years.

The Struggling Giants: The outlook is dimmer for the continent’s traditional economic heavyweights unless they reform rapidly:

- Angola: The oil exporter is dangerously over-exposed to the long-term decline of fossil fuels. Without a radical pivot to mining, services and manufacturing its outlook is bleak in a decarbonizing world; unfortunately, oil is set to remain the key economic driver for the foreseeable future.

- South Africa: Though energy supply has improved and blackouts ended under the coalition government that took power in 2023, the country still faces formidable challenges in the form of high crime and unemployment, outdated transport infrastructure and trade tensions with the U.S. Trump administration, which will hamper future economic growth.

Long-term population shifts

Looking further ahead towards mid-century, Africa’s economic potential is as vast as associated risks. The continent is undergoing a demographic seismic shift. By 2050, one in four people on the planet will be African. The working-age population will expand by approximately 700 million people. This is either a “demographic dividend” that could fuel a manufacturing boom similar to China’s, or a “demographic disaster” of mass youth unemployment and instability.

The AfCFTA Effect

The African Continental Free Trade Area (AfCFTA) is the wildcard. If fully implemented, the World Bank estimates it could lift 30 million people out of extreme poverty and boost income by $450 billion by 2035. It should also encourage value-added manufacturing; instead of exporting raw cocoa to Switzerland, Ghana could export chocolate to South Africa for instance. However, the risk is that countries are too slow to remove remaining barriers to trade, keeping the continent fragmented and unable to move up the value chain.

Technology as a Leapfrog

Technology offers a unique opportunity for Africa to bypass traditional development stages. We have already seen this with mobile money (M-Pesa), where Africa led the world. Fintech is democratizing access to capital for the unbanked. The next wave—agritech, telemedicine, and off-grid solar—could solve infrastructure deficits without the need for massive central planning.

Key Risks to Africa’s Economic Outlook

Despite the optimistic economic outlook for plenty of economies on the continent, three existential threats hang over Africa’s future.

- The Debt Trap: The era of cheap money is over. In the last decade, many African nations binged on Eurobonds and Chinese loans to fund infrastructure. Now, with global interest rates high and growth slowing, the bill is due. Countries like Zambia and Ghana have already defaulted; others like Kenya and Egypt are walking a tightrope. Debt servicing is crowding out vital spending. In 2024, many African nations spent more on interest payments than on health or education. This “debt overhang” threatens to usher in a new lost decade of austerity, where governments are forced to choose between paying foreign creditors and feeding their own people.

- Climate Change: Africa contributes the least to global warming (less than 4% of emissions) but suffers the most. The Sahel is heating up at 1.5 times the global average, driving desertification and fueling conflict between herders and farmers. Agriculture, which employs 60% of the workforce, is largely rain-fed and highly vulnerable to erratic weather patterns. Cyclones in the east and droughts in the south are becoming more frequent and severe. The economic cost is staggering; the African Development Bank estimates the continent is losing 5-15% of its GDP growth per capita annually due to climate change.

- Conflict and Instability: Peace is the prerequisite for profit. The recent wave of coups in the Sahel (Mali, Burkina Faso, Niger) and the devastating civil war in Sudan are reminders of the fragility of African states. Insecurity and an unstable political landscape act as massive taxes on growth, deterring foreign direct investment in Africa and destroying local markets. The spread of jihadist insurgencies in West Africa threatens to destabilize even the coastal success stories like Benin and Togo.

Conclusion

Africa is not a monolith; it is a mosaic. The question “Why is Africa poor?” is slowly being replaced by “Why is this African country succeeding while that one is failing?” The divergence is real. The path to prosperity is clear: economic integration through the AfCFTA, aggressive diversification away from raw commodities, and a relentless focus on good governance. The coming decades will determine whether Africa’s demographic boom becomes the engine of the global economy—or a source of global instability.