Overview of Argentina’s Current Economic Situation

Roughly two years have passed since Javier Milei took office as Argentinian president—two years which have seen a radical shift from the economic policies of the prior two decades. Milei inherited an unenviable situation, with inflation over 100%, a gaping fiscal deficit and GDP declining. His first year saw a particular focus on slashing public spending, reining in inflation and pushing through a raft of measures to liberalize the economy and reduce trade restrictions. Reform momentum stalled in his second year as the President looked to avoid rocking the boat before the October midterm elections, though the FX and monetary policy regime did see a significant overhaul. Below is a look at how key economic indicators have fared under Milei’s premiership.

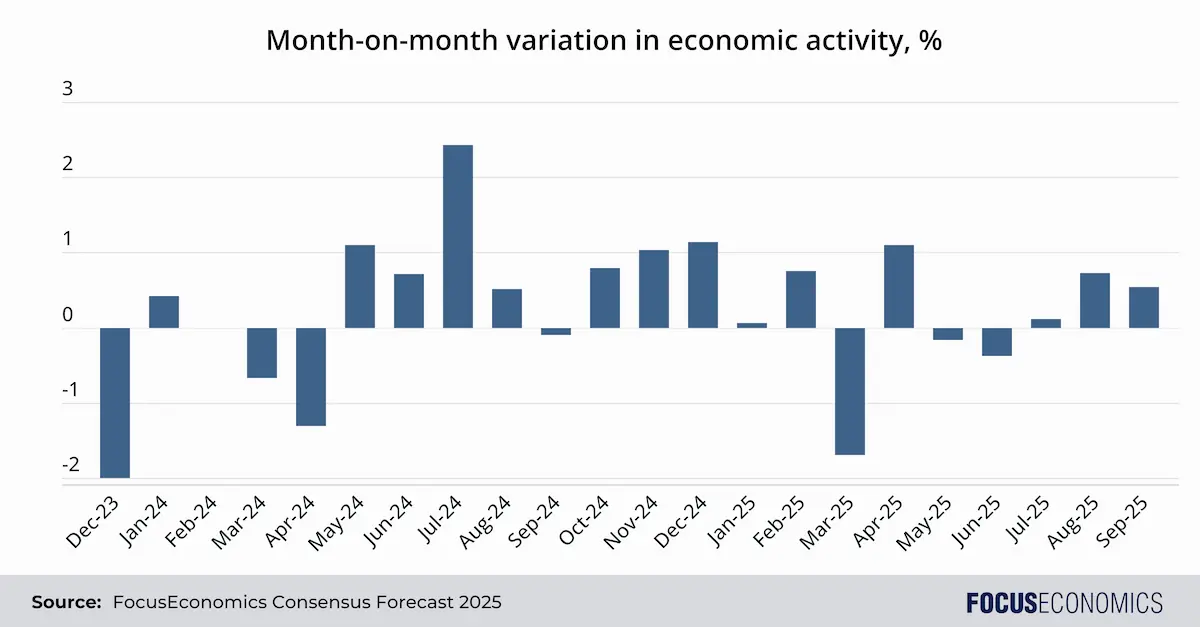

GDP growth

Harsh government spending cuts and surging inflation caused the economy to shrink steeply in the first few months of Milei’s presidency, before a recovery set in around mid-2024 as inflation and interest rates cooled and economic liberalization unshackled domestic demand. However, the economy has somewhat lost its way this year, with dry weather and the strong real-terms peso limiting exports, plus fears over the outcome of the midterm elections and interest rate volatility likely hampering investment.

Inflation

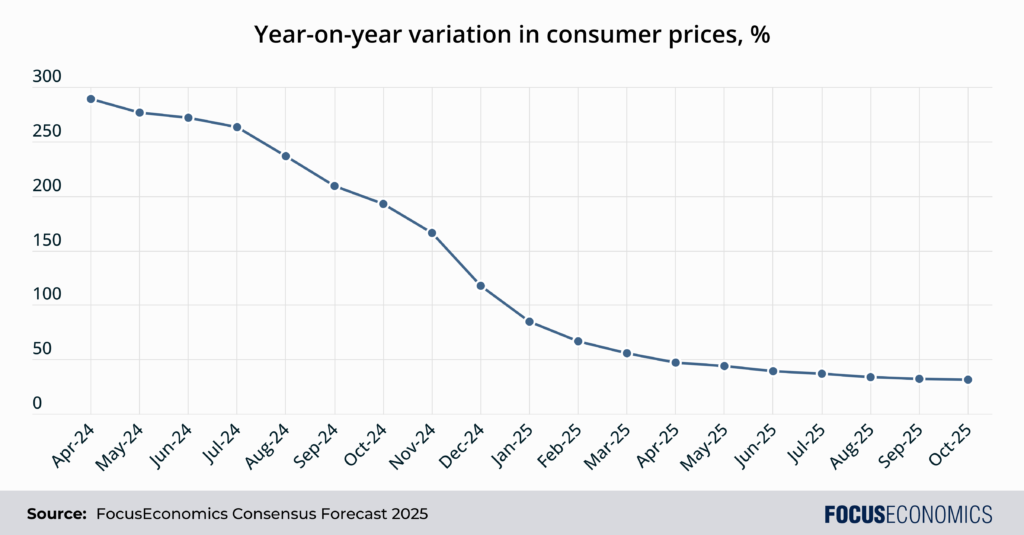

Milei has made taming prices a key goal of his administration, and year-on-year inflation has indeed declined continuously since its peak of nearly 300% in April 2024. However, the month-on-month change in prices has remained stubborn at around 2% so far in 2025, propped up by substantial peso weakening in nominal terms.

Fiscal balance

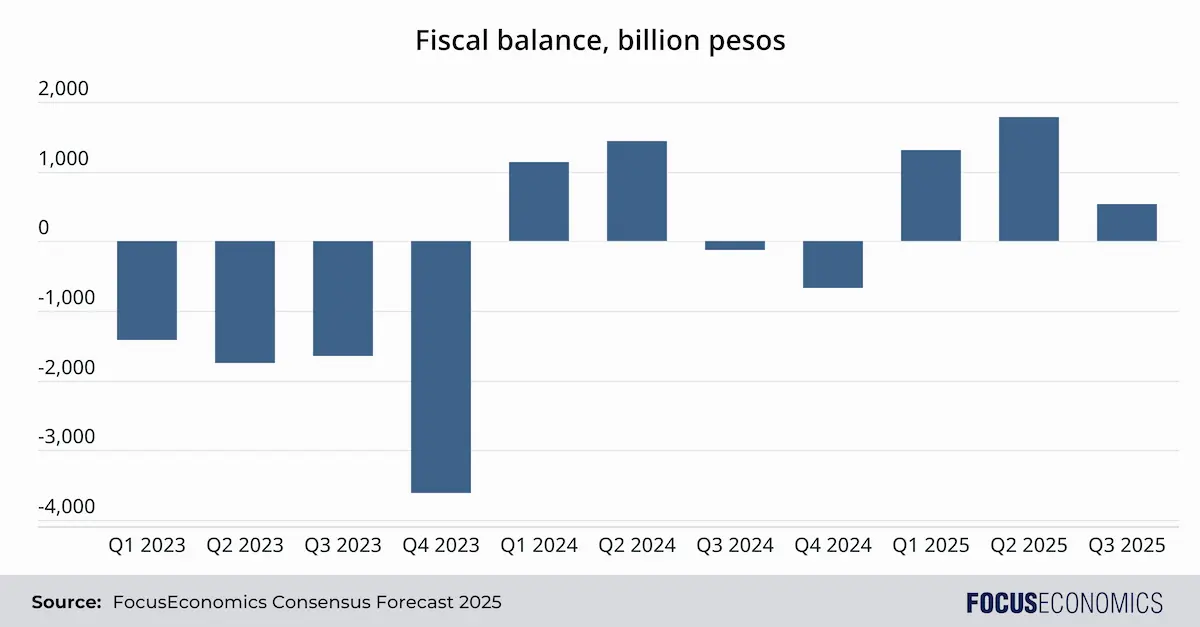

The government has run a fiscal surplus in most quarters since end-2023 as a result of tumbling government spending, marking a radical turnaround from the massive budget deficit incurred in 2023 due to pre-election fiscal giveaways by the previous administration.

Interest rates

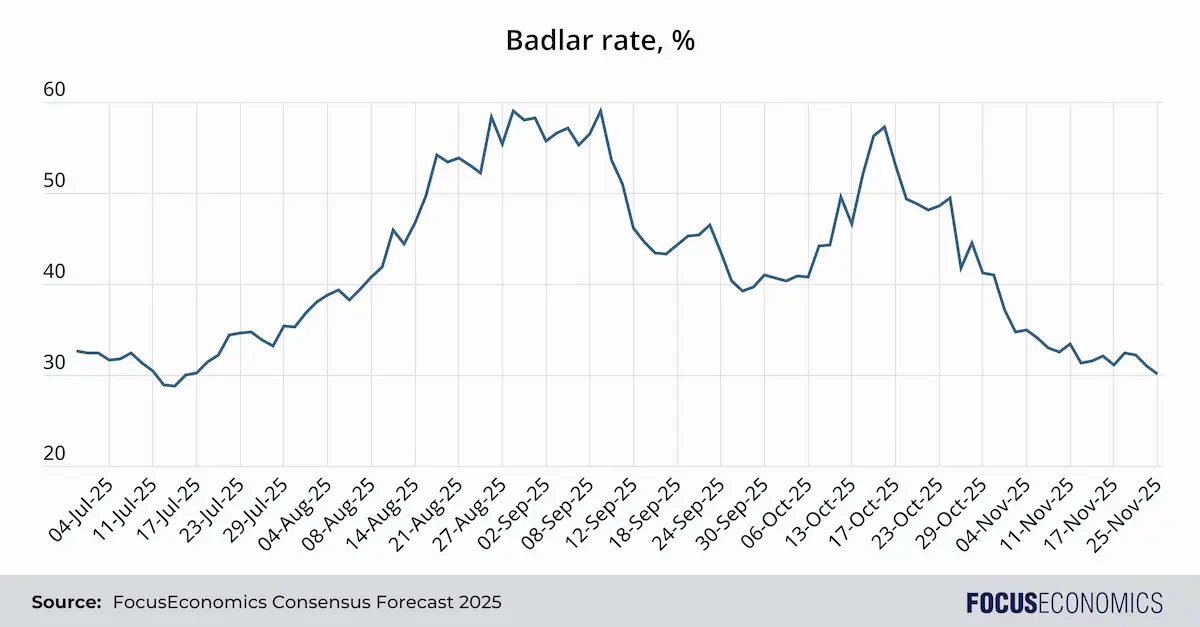

Milei’s time in office has been marked by frequent monetary policy adjustments. The Central Bank cut its main policy rate by 102 percentage points from December 2023 to January 2025. Lower interest rates helped boost credit to the economy; private-sector credit has risen by triple figures so far this year. However, the Bank abandoned its policy rate in July in favour of a monetary regime based on targeting the money supply. Since then, market interest rates have been extremely volatile due to fluctuating investor sentiment and associated Central Bank macroprudential changes, with the interbank badlar rate surging in the run-up to the October elections before tumbling since.

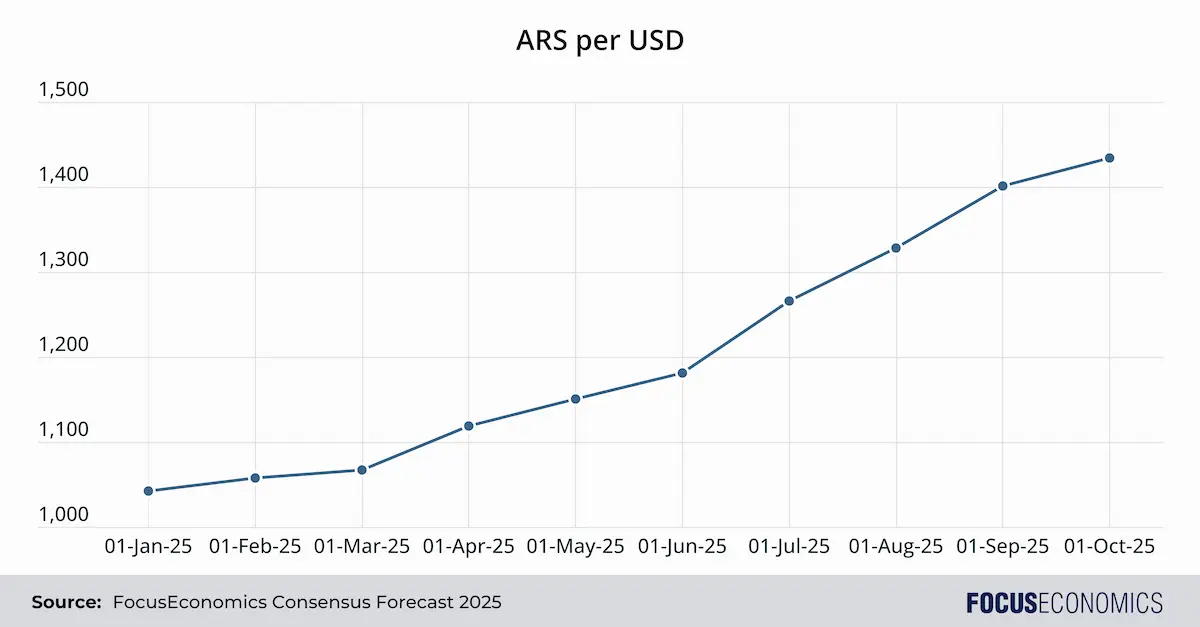

Exchange rates

There has only been one constant in Argentina’s exchange rate regime over the last two years: Constant change. Following a large currency devaluation in December 2023, Milei’s government initially allowed the official currency to depreciate by around 2% per month against the U.S. dollar. This rate was first reduced to 1%, then scrapped altogether in favor of a gradually widening trading band. As of late November 2025, the currency was near the top end of the trading band, having depreciated sharply since the middle of the year.

Key Economic Policies Implemented by Javier Milei

The President approved a number of reforms during his first year in office, mainly through two key bills: The “Ley Bases”, and an earlier “Decree of Necessity and Urgency”. Below is an overview of approved measures:

Deregulation and market liberalization

The authorities relaxed tenancy laws in order to boost the supply of rental properties, and tweaked employment rules in favor of employers in order to make the labor market less rigid. Moreover, the authorities have set the stage for several state-owned firms to be privatized, including the national flag carrier, Aerolineas Argentinas.

Tax reforms and fiscal policy changes

The government implemented a new regime to incentivize investment (RIGI). It includes tax and legal concessions to firms making large investments in strategic economic sectors such as energy, raw materials and technology. Moreover, the government eliminated some import restrictions, pared back public spending dramatically, and announced a tax amnesty that reportedly drew in around USD 18 billion to local banks shortly after the policy was introduced.

Impact of Milei’s Policies on Poverty and Inequality

Changes in poverty rates

Though Milei’s policies have been successful in some senses—they have helped to rein in inflation and boost credit for instance—they did lead to a temporary spike in the poverty rate, which rose to 53% in H1 2024 from 42% in H2 2023. That said, poverty then tumbled to just 32% in H1 2025, the lowest reading since 2018, as the economy recovered some lost ground.

Effects on the income distribution

Inequality figures have shown a similar picture: After spiking in early 2024, the gap between the incomes of the top and bottom income deciles has since narrowed somewhat. For instance, the gap rose from 19 times in Q1 2023 to 23 in Q1 2024 and back to 19 in Q1 2025.

Has Argentina’s economy improved under Milei?

Most available indicators suggest there has been some improvement in the economy’s health. The fiscal accounts have been brought back into balance. Public debt and inflation are both on a downward trajectory, and the economy is forecast to grow at one of the fastest rates in the region in 2025 as a whole despite some weakness in monthly economic activity readings. However, settling on a long-term, durable currency regime remains an outstanding task for the administration. A significant run on the currency in September–October 2025 was only staved off by a rare U.S. intervention in the FX market—hardly a sustainable solution to depreciatory pressure. To help the Central Bank accumulate reserves and avoid the currency becoming excessively overvalued, the country will likely need to move towards a more floating exchange rate—either by continuing to widen the currency tolerance band or doing away with it altogether.

Long-Term Prospects for Argentina’s Economy

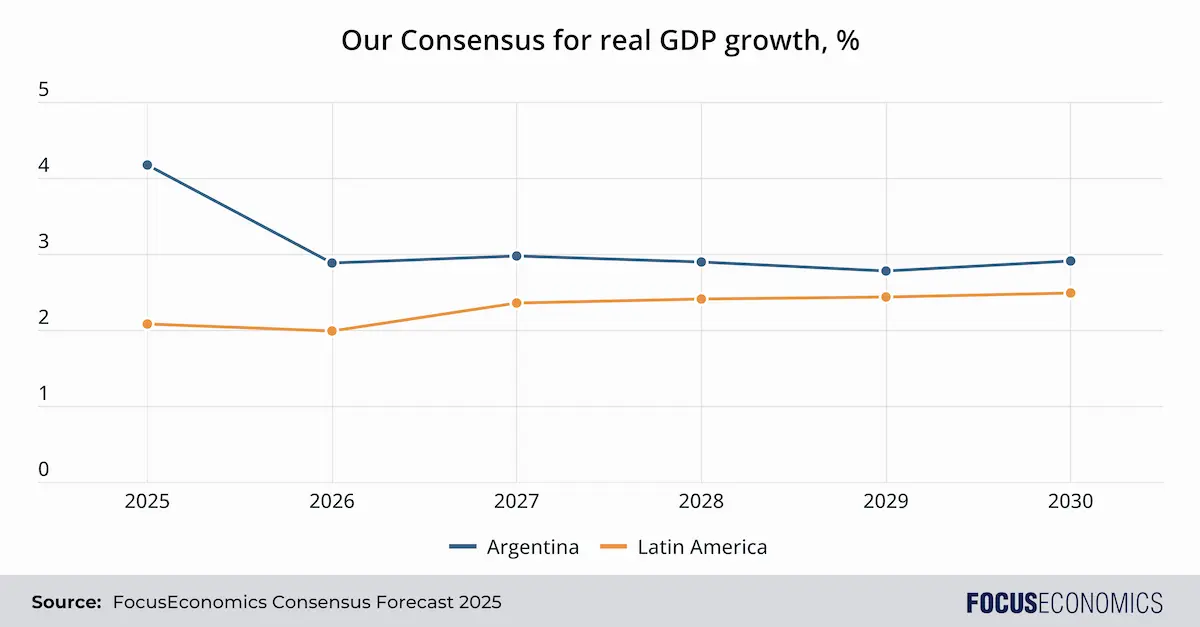

Our current Consensus is for Argentinian GDP growth to average around 3% per year out to 2030, contrasting the zero-growth recorded over the past decade and well above the Latin American average. As long as Milei remains in office, the economy is expected to benefit from declining inflation and interest rates. Moreover, the strong showing for Milei’s La Libertad Avanza party in the October midterm elections has boosted the prospects for further structural reforms to boost the business environment, with reforms to the tax and labor codes particular priorities. Meanwhile, strong relations with the U.S. government and financial support from the IMF should also anchor investor sentiment.

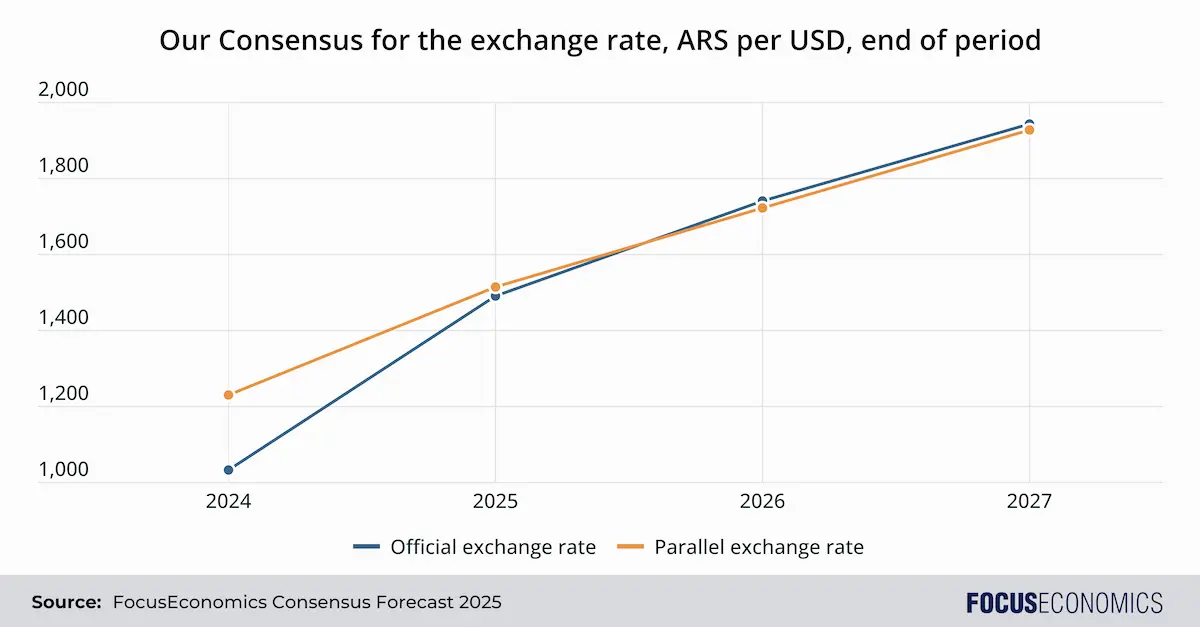

Our panelists expect the exchange rate to continue depreciating rapidly by international standards in the coming years, though the rate of depreciation should slow over time as inflation pulls back closer to the levels seen abroad. The gap between the official and parallel market rates—which has narrowed markedly since Milei took office—is expected to remain minimal as remaining currency controls are progressively loosened. Clarity regarding the steady-state currency regime and a public commitment not to use capital controls—which were partially reinstated in October to tame the slide in the peso—will be crucial to encouraging foreign investment and turning Argentina into a “normal” economy in outsiders’ eyes.

Risks abound. Chief among them is the prospect of a messy end to the current managed exchange rate regime leading to a collapse in the currency. Then there is an intensification of opposition from political and social groups; this will grow more likely if the economy doesn’t pick up and could test the sustainability of Milei’s economic reforms. Extreme weather is also an issue: Agricultural output collapsed by 24% in 2023 due to drought for instance. And, finally, a return to fiscal profligacy and inflation is on the cards if the Peronist movement wins the 2027 general elections. In short, at this stage—and given the country’s choppy past—it would still take a brave investor to go all in on Argentina’s economic future.

Insight from our analysts

EIU analysts commented on key economic drivers:

“Investment will be a major contributor to growth, owing to large investments in major projects related to mining and energy sectors under the Régimen de Incentivos para Grandes Inversiones (RIGI, an investment promotion regime). The government’s ambitious structural reform agenda, including privatisations and expanded remit of public private partnerships (PPPs), will bolster investment opportunities. Private consumption will also grow, owing partly to improved access to credit as interest rates fall, but also higher real salaries and a gradual improvement in employment. Net exports will also support growth as a weaker peso will encourage exports and weigh on the growth of imports.”

On reforms, Itaú Unibanco analysts said:

“Following the incumbent’s better-than-expected midterm results (see here), the government will likely push for greater momentum on a second phase of reforms. The “Bases” Law II, which builds on the bill approved in 2024 (see here), would include reforms to education, the labor market, natural resource exploitation, private property, and a tax framework. Importantly, President Milei recently met with most provincial governors (20 out of 24) to seek consensus on the reform agenda.”

On inflation, BBVA analysts said:

“The anti-inflation policy is on the right track, although challenges still lie ahead. Overall inflation (and even more importantly, core inflation) has accelerated since it hit its low of 1.5% in May. If the government maintains its fiscal and monetary commitment, inflation will tend to keep falling, but reducing it from these levels becomes more laborious. It will require the support of a solid monetary policy that maintains positive real interest rates (while also limiting their volatility), together with an exchange-rate policy that ensures greater strength in international reserves. This, in turn, will help make exchange-rate dynamics less vulnerable to external and/or political swings.”